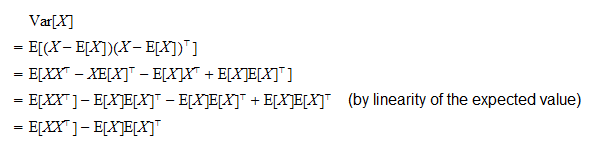

Dot Product Covariance Matrix

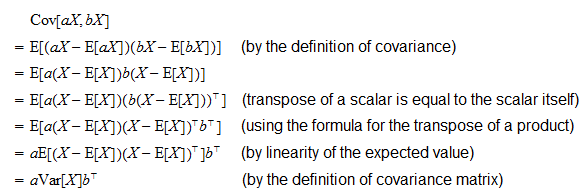

Z-scaling then dot product is proportional to the sample variance which is an estimator of the variance between the two variables. Conceiving of a μ a and b μ b as scaled vectors we can rewrite covariance as a dot product.

What Is Meant By A Covariance Matrix And Why Do We Use It Quora

33 X i R i e 1 Y i R i e 2 Z i R i e 3 where Ri is the data vector at the i th sample.

Dot product covariance matrix. Obviously cov x y cov y x. I just want to implement a function that given a matrix X returns the covariance matrix of X XTX which is just a simple matrix multiplication. Transpose of a Matrix Product.

In Tensorflow its gonna be easy. You get a covariance matrix similar to the one from the function npcov. One of the steps is to prove that sample covariance of residuals and the fitted values y_hat is zero.

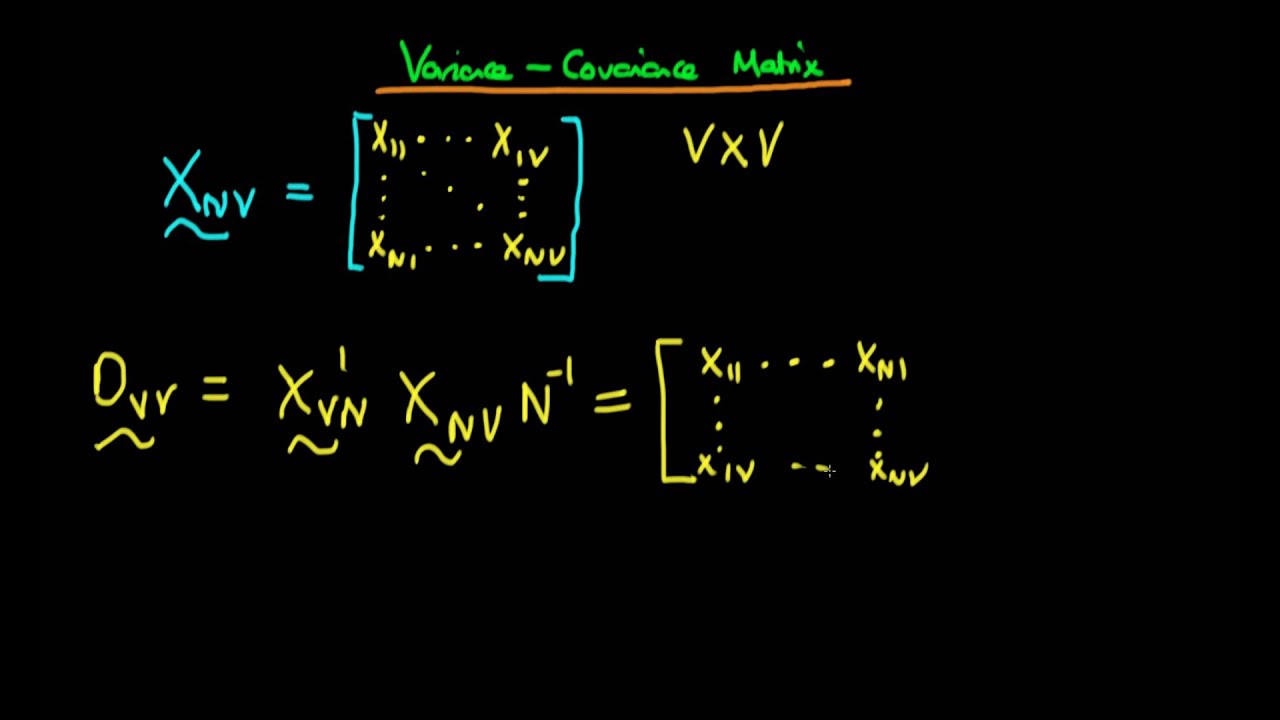

You get a covariance matrix similar to the one from the function npcov. The Covariance Matrix Definition Covariance Matrix from Data Matrix We can calculate the covariance matrix such as S 1 n X0 cXc where Xc X 1n x0 CX with x 0 x 1. Given an array w 1xN of weights and a covariance matrix Q NxN of assets one can calculate the covariance of the portfolio using the quadratic expression w Q w where is the dot product.

So the matrix is symmetric. The transpose of the dot product between two matrices is defined as follows. We compare this to the covariance computed using the dot product.

If the samples are conditioned so that sample means are zero eg. The dot product between the ones matrix and A matrix will result in a 5 x 3 matrix where each column contains the total of all marks accumulated for each subject which is. The other object to compute the matrix product with.

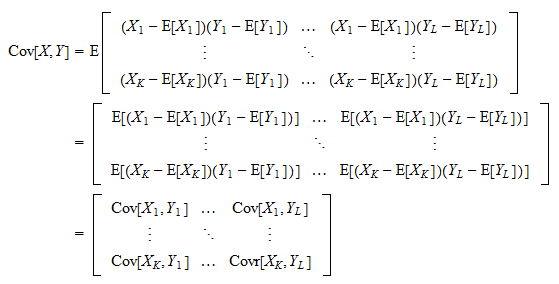

E1 e2 and e3 are the eigenvectors sorted in descending order of. The covariance of two random variables X and Y can be defined as EX-EX times Y - EY the covariance holds the properties of been commutative bilinear and positive-definite. These properties imply that the covariance is an Inner Product in a vector space more specifically the Quotient Space.

This method computes the matrix product between the DataFrame and the values of an other Series DataFrame or a numpy array. If X and Y are statistically independent then their covariance will be zero. This is important to keep in mind that the dot product of a matrix with its transpose corresponds to the covariance matrix.

Why two vectors covariance is the dot product of these two vectors 1 I am trying to understand the OLS property that SST Total sum of squares SSE explained sum of squares SSR residual sum of squares. This is important to keep in mind that the dot product of a matrix with its transpose corresponds to the covariance matrix. X p denoting the vector of variable means C In n 11n10 n denoting a centering matrix Note that the centered matrix Xc has the form Xc 0 B B B B B x11 x 1 x12 x2 x1p x p x21 x1 x22 x 2 x2p x p x31 x1 x32 x 2 x3p x p.

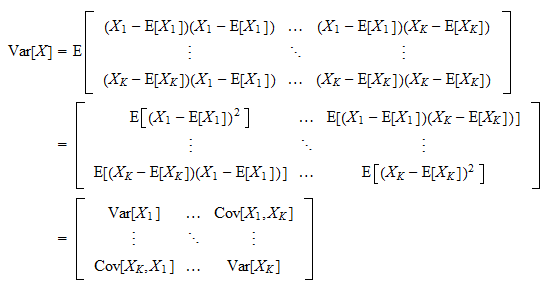

I want to understand what is the best way to perform this operation when I have an history of weights W T x N and a 3D structure for covariance matrix T N N. Cov a b a μ a b μ b N We can calculate covariance in R using the cov function. Covariance Matrix The variance and covariance both being merely dot products can be summarized in a single matrix.

The APIs in Keras like multiply and dot dont fit my request. It can also be called using self other in Python 35. TfmatmulX tftransposeX But I didnt expect that its a nightmare with Keras.

Association with the kernel trick. Compute the matrix multiplication between the DataFrame and other. This is easily achieved by forming the dot product of the data vector with the three eigenvectors of its covariance matrix.

Correlation The Sample Covariance Matrix Where The Sample

Why Is The Eigenvector Of A Covariance Matrix Equal To A Principal Component Mathematics Stack Exchange

Techniques For Studying Correlation And Covariance Structure Ppt Video Online Download

Covariance Matrix

A Covariance Matrix For Three Traits A B And C The Diagonal Download Scientific Diagram

Covariance Matrix

Covariance Matrix

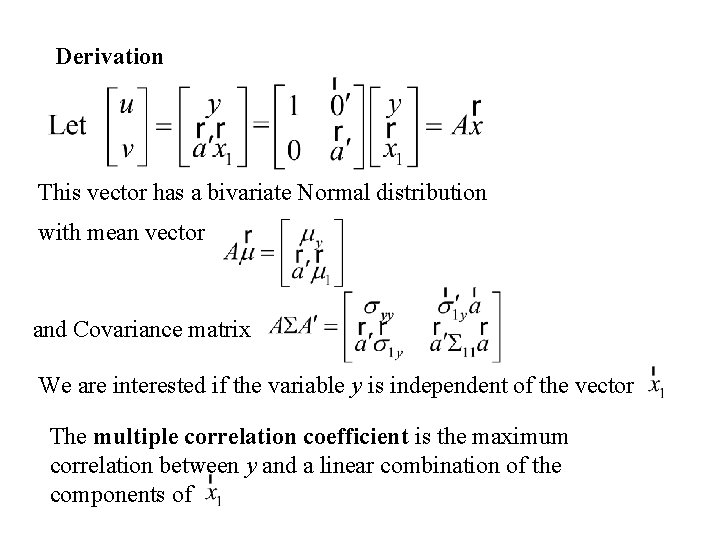

The Multiple Correlation Coefficient Has P 1 Variate Normal Distribution With Mean Vector And Covariance Matrix We Are Interested If The Variable Ppt Download

Baffled By Covariance And Correlation Get The Math And The Application In Analytics For Both The Terms By Srishti Saha Towards Data Science

Understanding The Covariance Matrix Datascience

How To Interpret An Inverse Covariance Or Precision Matrix Cross Validated

Understanding The Covariance Matrix Datascience

A Covariance Matrix For Three Traits A B And C The Diagonal Download Scientific Diagram

Correlation The Sample Covariance Matrix Where The Sample

Covariance Matrix

Understanding The Covariance Matrix Datascience

Http Rinterested Github Io Statistics Covariance Html

Covariance Matrices Covariance Structures And Bears Oh My The Analysis Factor

Variance Covariance Matrix Using Matrix Notation Of Factor Analysis Youtube